Next week sees the end of the 2016-17 tax year. On the 6 April 2017, any action you take to minimise your tax liabilities for 2016-17 will be largely ineffective. So what, if anything, can you still action this week?

Capital gains tax (CGT)

The amount of tax free gains you can make during 2016-17 is £11,100. This exempt allowance is available to all UK resident tax payers, accordingly, married couples and civil partners both qualify.

If you have no gains chargeable to CGT thus far during 2016-17, there is still an opportunity to crystallise gains during this coming week, up to the annual exemption limit, and no tax will be payable. For example, if you have a shareholding that you have been considering for disposal, and you could sell a sufficient quantity of shares before 6 April 2017, the disposal would utilise your allowance without creating a tax liability.

The important matter to note is that this annual exemption is lost if you don’t use it; it cannot be carried forward and used in later years.

Inheritance tax (IHT)

There are a number of annual reliefs that you can use without creating a chargeable event for IHT purposes. For example, the exempted annual gifts you can make are:

You can give away £3,000 worth of gifts each tax year (6 April to 5 April) without them being added to the value of your estate. This is known as your ‘annual exemption’.

You can carry any unused annual exemption forward to the next year – but only for one year.

Each tax year, you can also give away:

- wedding or civil ceremony gifts of up to £1,000 per person (£2,500 for a grandchild or great-grandchild, £5,000 for a child)

- normal gifts out of your income, for example Christmas or birthday presents – you must be able to maintain your standard of living after making the gift

- payments to help with another person’s living costs, such as an elderly relative or a child under 18

- gifts to charities and political parties

You can use more than one of these exemptions on the same person – for example, you could give your grandchild gifts for her birthday and wedding in the same tax year.

Small gifts up to £250

You can give as many gifts of up to £250 per person as you want during the tax year as long as you haven’t used another exemption on the same person.

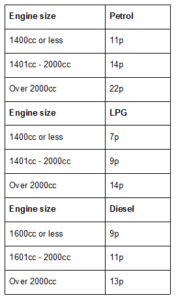

Company car users

If your employer pays for your private fuel this will create a fairly significant income tax charge for 2016-17. You may save money if you calculate the cost of the fuel provided and reimburse your employer. For 2016-17, you need to do this before 6 April 2017. (For 2017-18, the rules are being relaxed slightly and you will have until 6 July 2018 to make an equivalent reimbursement for 2017-18).

To make the calculation you will need your private mileage for 2016-17 and multiply this by the advisory fuel rate for your vehicle. These range from 7p to 22p per mile. See the published list at https://www.gov.uk/government/publications/advisory-fuel-rates/advisory-fuel-rates-from-1-march-2016

These are just a few of the actions you could take to minimise your tax payments during what’s left of 2016-17. If you are unsure what your options may be, please call, we would be delighted to help.